Choose the Right One Credit Card for You

Discover powerful strategies for using cash back rewards credit cards effectively. This guide equips you with the knowledge to boost your earnings and make the most of your card.

Latest News

Best Western Bonus Points: Stay & Earn up to $100!

Best Western Rewards members can earn 10,000 bonus points (worth $50) for a 3-night stay or…

Amazon PepsiCo Deal: $5 Off $20+

Snag $5 off $20+ of select PepsiCo products on Amazon! Maximize savings with rewards cards &…

Sky Blue MacBook Air (2025): M4 Chip, 16GB RAM Deal!

Snag the Apple MacBook Air (2025) in Sky Blue for just $837.19! This deal includes an…

IHG Points Sale: 100% Bonus, 0.5¢ Per Point!

Buy IHG points with a 100% bonus! Get points for 0.5¢ each. Limited-time offer. Maximize savings…

Costco Apparel Deal: Save $30 on 5+ Items!

Costco offers two apparel promotions: save $10 on 3+ items or $20/$50 on 5-9/10+ items! Limited…

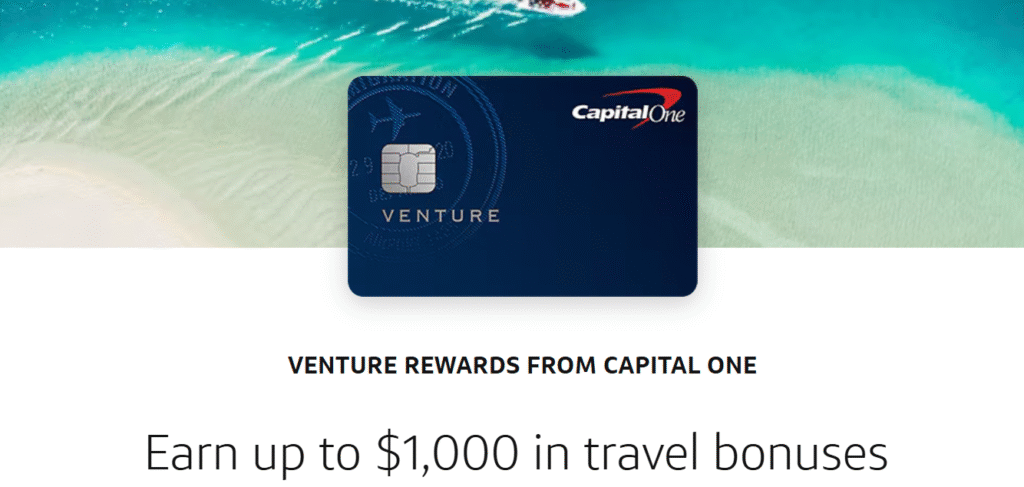

Capital One Venture Card: 75K Miles + $250 Travel Credit (Expiring Soon!)

Capital One Venture Card offers 75K bonus miles + $250 travel credit. Earn 2X miles on…

Most Popular Posts

Stay Always In Touch!

Subscribe To Our

Newsletter.

Find the card that rewards you for what you actually spend on.