A group of crypto investors failed to buy a first printing of the U.S. Constitution Fees face-off The battle between the world’s largest e-commerce company and the world’s largest payments network started quietly. It began in Singapore, wherein September Amazon.com Inc. started adding a small surcharge to any purchases made […]

Updated on Tuesday, November 23, 2021 A Roth IRA can be an excellent way to set money aside for retirement, but knowing how to make your money grow in a Roth IRA can be confusing. The first thing to understand about Roth IRAs is that they don’t have their own […]

Updated on Monday, November 22, 2021 Checking accounts are a safe and convenient place to store your money for everyday financial transactions, allowing you to withdraw funds to make purchases or to get cash from ATMs whenever you’d like. Many checking accounts have different types of fees, but some financial […]

Is the American Express® / Business Extra® Corporate Card the right credit card to meet your business travel needs? American Express disclaimer American Express As you’re growing your business, having the right credit card can make a world of difference. And for companies with large travel expenses, the potential savings […]

Updated on Monday, November 15, 2021 Individual retirement accounts (IRAs) are investment accounts with tax benefits that are specifically designed to help you save and grow money for retirement. There are several types of IRAs and they differ mostly due to tax implications. A traditional IRA is one of the […]

If you’re looking to save more money beyond your regular savings account, consider adding a money market account (MMA) to the mix. A money market account can earn at a higher rate than a savings account, especially if you have a larger balance to deposit. Many MMAs tier their rates […]

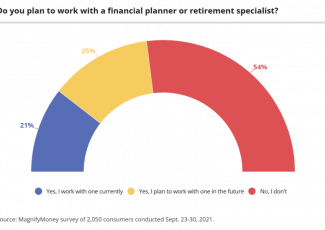

Updated on Monday, November 8, 2021 They don’t call them the golden years for anything — American consumers spend much of their lives working toward retirement, so many have probably thought about their ideal retirement and how to make it happen. MagnifyMoney researchers set out to identify what a dream […]

There is no wax on wax off for saving money. You learn to keep aside a chunk of your earnings gradually. You should not get complacent with your salary – it doesn’t mean that you don’t earn enough to start saving. Even if your salary is equal to the proverbial […]

How can you save money on car insurance? Simply park your car in the garage at night and get a discount on your car insurance! Weird, right?! Well, this read is full of weird and lesser-known facts which help you in saving money on car insurance. I know for a fact […]

Turning a Medical Emergency into a Financial Emergency is definitely not a smart move. So, to be financially stable when in need of any medical attention you definitely need Health Insurance. But, if you’re new to Health Insurance then you might find that in the United States Health Insurance is […]

Tags: amazon cashback rewards credit card, Amazon Prime Rewards Visa Cards, Amazon Rewards Visa Cards, Amazon Visa Card Apply, Amazon Visa Card Como Funciona, Amazon Visa Card Credit Score, Amazon Visa Card Credit Score Needed, Amazon Visa Card Sign Up Bonus, Amazon Visa Cards, Amazon Visa Signature Cards, Are Amazon Visa Gift Cards Safe, best cashback rewards credit card, best rewards credit cards, crypto investors, Do Visa Cards Work On Amazon, Does Amazon Sell Visa Cards, Does Amazon Take Visa Cards, rewards, top cashback rewards credit cards, Using Visa Cards On Amazon, Visa Cards, Visa Playing Cards Amazon